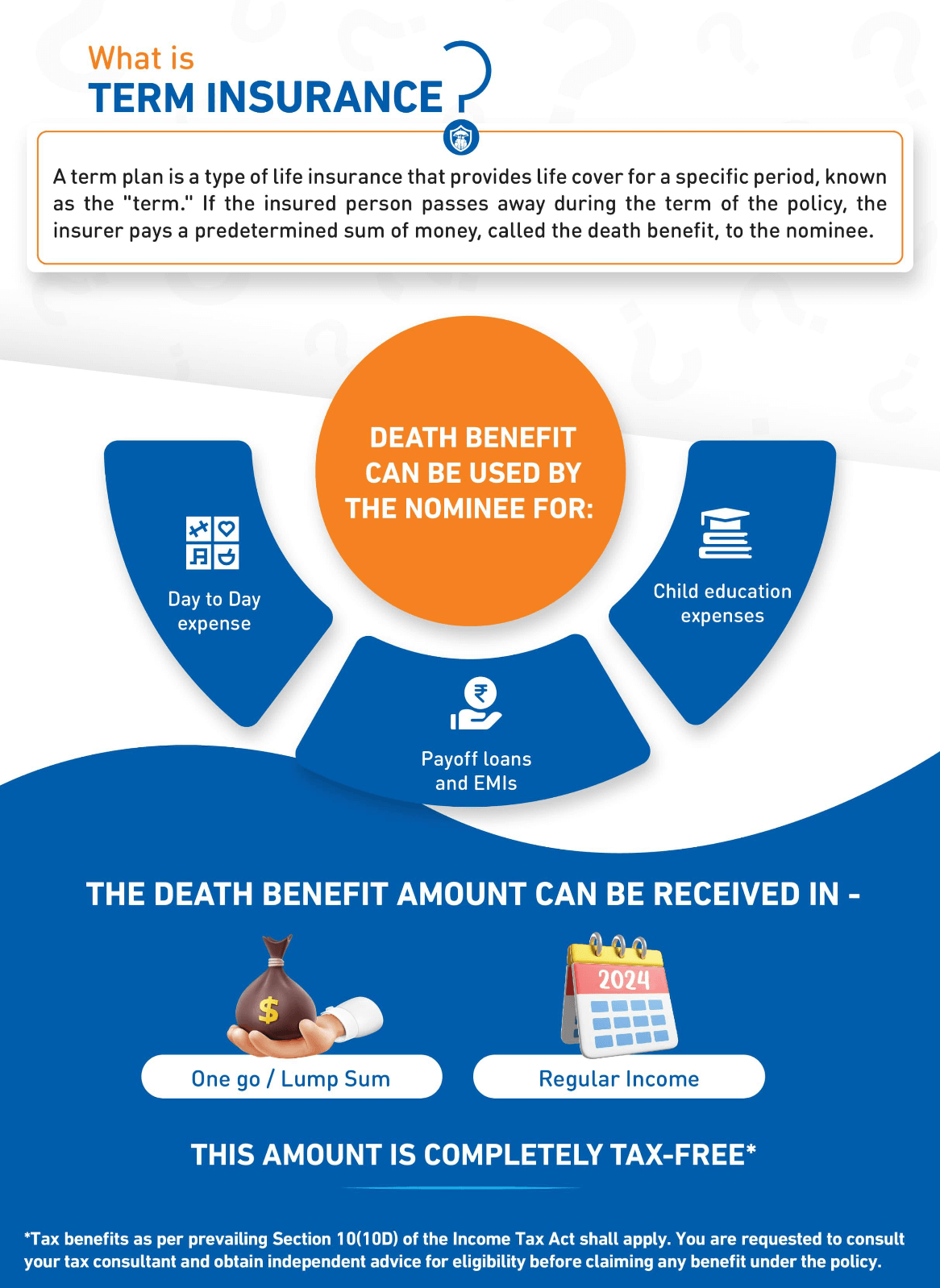

Term insurance is a pure form of life insurance plan which provides financial protection to the life assured’s nominee(s) in case of the demise of the life assured during the policy tenure. It involves an agreement between the policyholder and the insurance company, wherein the insurer provides a life cover to the life assured for which he/she pays the premium to the insurer. The term plan is for a specific tenure. If the life insured dies during the selected tenure, the insurance company pays the sum assured to the family to help them deal with the expenses or debts, if any, due to the loss of the earning member of the family.

Palak Bagadia, Associate – Digital Marketing at Bajaj Life Insurance, with experience spanning content and performance marketing, recruitment, employee engagement in the BFSI industry, with a strong understanding of the insurance sector.

Reviewed ByAvdhesh Gupta

AboutAvdhesh Gupta

Avdhesh Gupta, Appointed Actuary at Bajaj Life, brings close to 20 years of experience across life insurance, reinsurance and consulting. He plays a key role in strengthening risk governance, ensuring long-term financial sustainability, and driving customer and shareholder value. He oversees actuarial and risk functions, including valuations, embedded value, product pricing, regulatory and shareholder reporting, and enterprise risk management. Avdhesh also leads global reinsurance partnerships and serves on the Advisory Group of the Institute of Actuaries of India on IFRS 17

Check out this video to understand What is Term Insurance and Why you need one?

For example, say Mr Sharma buys a term plan for his life. He chooses a sum assured of Rs. 50 lakhs and a policy term of 30 years. After 10 years, he died due to an accident. In this case, the family will receive Rs. 50 lakhs as the death benefit on Mr Sharma’s death, subject to terms & conditions specified in the policy.

It guarantees* the sum assured on the insured’s demise during the term of the policy, provided all due premiums are paid. As such, if the insured dies prematurely, the family is compensated for any financial loss that they may have suffered, to the limit of the sum assured under the plan. They might meet their lifestyle needs and also might fulfil their financial obligations/goals even when the breadwinner is not around. This brings out the term insurance meaning and makes it an important component of your portfolio for emergency planning.

Why is Term Insurance Important?

Now that you know the term insurance definition, find out why the plan proves essential in financial planning:

Financial protection for your family.

When you are the only earning member, your family relies on your income for everyday expenses and future goals. Term insurance helps them stay financially stable if life takes an unexpected turn.

Protect Your Assets

If you have financial commitments, such as a home or car loan, term insurance can help your family pay them off. This ensures the assets you built remain secure.

How Does Term Insurance Work?

Now that you know what term insurance is and its importance. Let's now focus on how term insurance works step by step, with a simple example

Step 1: Choosing the Coverage

Ajay, a 32-year-old working professional, wants to secure his family’s financial future. He decides to buy a term plan with a ₹1 crore sum assured so his family can manage expenses, loans, and future goals if something happens to him.

Step 2: Selecting the Policy Term

Ajay chooses a 25-year policy term depending on his coverage needs.

Step 3: Premium Calculation

The insurance company calculates Ajay’s premium based on his age, health, lifestyle, and life expectancy. In some cases, insurers may ask for a medical test to review his health and family medical history. Ajay can also use a term insurance premium calculator to estimate his premium before buying the policy.

Step 4: Paying the Premium

Ajay pays his premium regularly throughout the premium-paying term to keep the policy active.

Step 5: Protection During the Policy Term

For the next 25 years, Ajay’s life remains covered. He can also choose to add on riders like accidental death benefit rider, critical illness benefit rider , etc., at an additional nominal cost to get additional coverage

Step 6: Claim and Payout

If Ajay passes away during the policy period, his nominee will receive the coverage amount. A high claim settlement ratio indicates a higher probability of claims being honoured.

Step 7: If the Policy Term Ends

If Ajay survives the full policy term, the coverage ends, there is no payout unless he has chosen a return-of-premium option. Ajay may also renew the policy, though the premium may be higher because it will be based on his age at the time of renewal.

Key Features of Term Insurance Plans

Check out this video to understand Benefits or Key features of Term Insurance

Riders and Add-Ons

Term insurance plans allow you to customise your coverage through additional riders. Popular options include accidental death benefit, critical illness cover, waiver of premium, accidental death benefit, family income benefit etc.

Tax Advantages

When you pay premiums for a term insurance plan, you can claim tax deductions of up to ₹1.5 lakh under Section 80C, in case of old tax regime. The payout your family receives is usually tax-free under Section 10(10D), subject to certain conditions.

Eligibility and Entry Criteria

Eligibility varies slightly across insurers, but most plans allow entry between 18 and 65 years. If you buy early, you can lock in lower premiums and choose a longer policy term.

Payout Choices

You can also decide how your family should receive the payout. The sum assured can be given as a lump sum, as a regular monthly income.

Flexibility and Extended Coverage

Term insurance gives you the flexibility to pick a policy term that matches your financial needs. If you are just starting your career, you may opt for longer coverage, while if you are closer to retirement, you may choose a shorter term. You can also choose to renew your policy once the term ends, though premiums may increase with age.

What are the Different Types of Term Insurance Plans in India?

Now that you know what is term insurance, here’s a look at the different types of term insurance plans that are available in the market.

Type

Term Plan Meaning

Level Term Insurance

Under this type of plan, the sum assured remains constant throughout the policy term. If the life insured dies during the policy term, the insurer pays the sum assured and the plan terminates.

Increasing Term Insurance

Under this type of plan, the sum assured increases every year. If the insured dies during the policy term, the increased sum assured at the time of death is paid, and the plan is terminated.

Decreasing Term Insurance

Under this term plan, the sum assured reduces every year on a pre-defined basis. If the life insured dies during the policy term, the reduced sum assured at the time of death is paid, and the plan is terminated.

Term Plan with Return of Premium

This term plan has a maturity benefit and is different from other plans. Under this plan, if the life insured dies during the policy term, the sum assured is paid. However, if the insured survives the policy tenure, the premium paid after deducting applicable taxes is refunded back as a maturity benefit, provided all the premiums of the plan are duly paid.

How to Choose a Term Insurance Plan?

Check out this video to understand How does a Term Plan Work?

When you look to buy the plan, there will be multiple options for you to choose from. In order to get the best term insurance plan based on your coverage needs, here are some factors that you may consider:

Type of policy

First, determine the type of policy that suits your needs. As mentioned earlier, there are different types of term plans. Assess these plans and choose one that matches your coverage needs.

For instance,

If you want uniform coverage throughout the policy duration, choose a level term plan

If you want the sum assured to increase with your increasing financial responsibilities, you can opt for an increasing term plan

If you have a loan, for example, and you want a plan to cover the reducing balance of the loan, you can choose a decreasing term plan

If you are looking for maturity benefit too, a term plan with a return of premium term plan will be the most suitable one.

The Sum Assured

Having optimal coverage is essential for financial security. So, opt for a suitable sum assured. To assess a suitable sum assured, you can use the term insurance coverage calculator. These calculators help you estimate the optimal sum assured so that you are optimally insured, and your family gets the required financial assistance in the case of emergencies.

Optional riders

Term insurance plans allow a range of optional riders to enhance coverage, on payment of an additional nominal premium. For instance -

The Accidental Death Benefit rider pays an additional financial coverage in case of accidental death during the policy term

A critical illness insurance rider offers financial coverage in case the insured person is diagnosed with any of the illnesses covered.

The Waiver of Premium Benefit Rider ensures that all future premiums are waived off if the insured person is unable to pay them due to accidental permanent disability or a critical illness diagnosis.

So, based on your coverage needs, choose the suitable riders and enjoy a wider scope of coverage on payment of an additional nominal premium.

Claim Settlement Ratio

The Claim Settlement Ratio (CSR) defines the percentage of claims the insurance company has settled against the total claims received by it in a financial year. The higher the ratio, the better the probability that the insurance company will make the claim settlements. So, compare the CSRs of different insurers, and you may opt for the one that has a high ratio.

Premium v/s Coverage

The suitable term insurance policy will be the one that offers an inclusive scope of coverage as per your needs at an affordable premium.

Understand what is term insurance, how it works and its importance. Use the aforementioned parameters and buy a suitable policy that matches your coverage needs. Secure yourself and your family financially against unforeseen eventualities.

Factors to Consider Before Buying a Term Insurance Plan

Here is what you should look at before finalising your decision to buy a term insurance policy

Financial Protection Against Uncertainties

Choose a coverage amount that can support your family’s future needs. The sum assured should ideally help them manage daily expenses, pay off any outstanding liabilities and achieve long-term goals.

You can use this formula to estimate the coverage required

Meet Amit, a 34-year-old professional with a spouse and one child. His monthly household expenses are Rs. 40,000. Here’s how he calculated the coverage he required,

Component

Calculation

Amount

Monthly Expenses × 150

₹40,000 × 150

₹60,00,000

Liabilities (+)

Home loan and credit card dues

₹20,00,000

Liquid Assets (−)

Fixed deposits and mutual funds

− ₹10,00,000

Future Expenses (+)

Child’s higher education and major life goals

₹20,00,000

Spouse Retirement Corpus (+)

Financial support for spouse’s retirement

₹10,00,000

Total Estimated Insurance Cover Needed: ₹1 Crore

Coverage for Critical Illnesses

Some term plans allow you to add a critical illness benefit rider. This provides financial support if you are diagnosed with any of the critical illnesses mentioned in the rider document

Accidental Death or Disability Rider

You can also include accidental death or disability riders in your plan. It provides additional financial support if an accident leads to death or permanent disability.

Steps to Buy Term Insurance Online

Step 1: Understand Your Financial Needs

Start by thinking about your family’s financial needs. Look at your monthly expenses, loans, number of dependents, and future goals like children’s education so you can choose a coverage amount that truly supports them.

Step 2: Check the Term Insurance Premium

Your premium depends on factors like your age, coverage amount, policy term, and lifestyle habits. You can use a term insurance premium calculator to get an estimate of how much the plan may cost.

Step 3: Choose Suitable Riders and Add-ons

You can strengthen your policy by adding riders such as critical illness cover, accidental death benefit, or family income benefit. Pick the ones that match your financial needs so your family gets better financial protection.

Step 4: Buy the term insurance Plan Online

Buying a term plan online is quick and convenient. You can get a ₹1 crore term insurance plan for premiums starting at just ₹14 per day.*

Key Takeaway

Term insurance is a pure protection plan that provides financial support to your family if the life assured passes away during the policy term.

It offers comprehensive life cover at an affordable premium, helping your family manage daily expenses, loans, and future goals.

You pay a fixed premium for a chosen policy term, and the insurer pays the sum assured to the nominee in case of death of life assured during that period.

Term plans also allow additional financial protection through riders such as critical illness benefit rider , accidental death benefit rider, or waiver of premium rider.

Premiums and coverage depend on factors like age, health, lifestyle habits, and policy duration.

Choosing the right coverage amount and insurer with a good claim settlement ratio helps ensure strong financial protection for your family.

Conclusion

Term insurance is a simple and affordable way to protect your family’s financial future. By choosing the right coverage amount and policy term, you can ensure your loved ones have the support they need to manage expenses, repay loans, and stay financially secure if life takes an unexpected turn.

How does a term insurance policy work in case of death during the policy term?

If the life assured passes away during the policy term, the nominee files a claim with the insurer, and after verification, the insurance company pays the sum assured to the nominee as the death benefit.

Does term insurance coverage end after the policy term?

Yes, the coverage ends once the policy term is completed.

How do I calculate the right amount of term insurance coverage for my needs?

Alternatively, you can also use an online term insurance coverage calculator to quickly estimate the coverage amount based on your financial details.

Do I get my money back in a term insurance plan?

No. A pure term insurance plan does not offer any maturity benefit if you survive the policy term. This is because term insurance is designed to provide pure life cover with no savings/investment benefits. However, if you choose a term plan with return of premium, you can get the premiums back as per policy terms and conditions.

What is the best age to buy term insurance?

There is no ideal age to buy term insurance, but the younger you are when you purchase a policy, the lower your premium is likely to be. Buying early can help you secure higher coverage at an affordable premium, as you are at a lower risk.

Which is better, life insurance or term insurance?

Life insurance is a broad category of life insurance products, and term insurance is one of the type of life insurance. Term insurance offers pure financial protection for a specific period with a high sum assured at affordable premiums. Other life insurance plans, such as whole life, endowment, or ULIP plans, combine life cover with savings or investment benefits. The right choice depends on your financial goals. If you want affordable, high-value protection, term insurance may be suitable. If you want life cover along with savings or wealth creation, you may consider other life insurance plans.

Can I change nominee later in a term insurance?

Yes, you can change your nominee in a term insurance plan any time during the policy term. You can update your nominee information when a major life event occurs, like marriage, divorce, childbirth, or the death of an existing nominee.

How often should I review my term policy?

It is good to review your term policy at regular intervals, whenever there is a major life change, like marriage or childbirth. This helps ensure your life cover remains adequate for your current life situation and future goals.

Can I buy term insurance after 40?

Yes, you can buy term insurance after 40. It can help financially secure your dependents, clear loans, and cover future goals in your absence. Use the Human Life Value (HLV) method to find the right coverage based on your income, liabilities, and future financial goals before buying a policy.

Can I increase my term insurance cover later?

Yes. If you choose an Increasing Life Cover or Life-Stage benefit option at the time of purchase, you can increase your life cover later. With Life-stage benefits, you can enhance the cover during a major life event, such as marriage or childbirth. In an Increasing Term Plan, your sum assured grows at regular intervals during the policy term.

Can I buy term insurance if I have a pre-existing condition?

Yes, you can buy term insurance if you have a pre-existing condition like high blood pressure, heart disease, or obesity etc. But you must disclose your pre-existing condition when applying for the policy. Based on your medical history, the insurer decides the premium and coverage they can offer.

The views stated in this article are not to be construed as investment advice and readers are suggested to seek independent financial advice before making any investment decisions. For more details on risk factors, terms and conditions please read the sales brochure & policy document (available on www.bajajlifeinsurance.com) carefully before concluding a sale. Bajaj Life Insurance Limited (Formerly known as Bajaj Allianz Life Insurance Company Limited) Reg. Office Address: Bajaj Insurance House, Airport Road, Yerawada, Pune - 411006. CIN: U66010PN2001PLC015959, call us on Customer Care No. 020-6712 1212, mail us on: customercare@bajajlife.com. The Logo of Bajaj Life Insurance Limited is provided on the basis of license given by Bajaj Finserv Ltd. to use its “Bajaj” Logo.

Tax benefits as per prevailing Section 11 (read with Schedule II, Sr.No.2) and Section 123 (under old tax regime) of the Income Tax Act shall apply. You are requested to consult your tax consultant and obtain independent advice for eligibility before claiming any benefit under the policy.

*Conditions Apply – The Guaranteed benefits are dependent on policy term, premium payment term availed along with other variable factors. For more details, please refer to sales brochure.

**Above illustration is for Bajaj Life eTouch II - A Non-Linked, Non-Participating, Individual Life Insurance Term Plan (UIN:116N198V07) considering Male aged 23years | Variant-Life Shield|Non-Smoker | Policy Term(PT)– 30 years | Premium Payment Term (PPT)– 30 years | Sum Assured opted is Rs.1,00,00,000 | Online Channel | Standard Life | 1st Year Premium is Rs. 4,775. 2nd Year onwards premium Rs. 5,176. Total Premium Rs. 1,54,879| Medical Rates | Yearly Premium Payment Mode | Death benefit opted is lumpsum payout and monthly instalments (Lumpsum Payout Percentage: 40, Income Payout Percentage: 60). Income payout instalment opted for 40 years | Premium shown above is inclusive of Online Discount and exclusive of any extra premium and is for illustrative purpose only. For more details on risk factors, terms and conditions please read sales brochure & policy document (available on www.bajajlifeinsurance.com) carefully before concluding a sale.

*Tax benefits as per prevailing Section 10(10D) and Section 80C of the Income Tax Act shall apply. You are requested to consult your tax consultant and obtain independent advice for eligibility before claiming any benefit under the policy.

~Individual Death Claim Settlement Ratio for FY 2023-2024

1Premium Holiday has to be selected at inception to avail this benefit and also depends on other policy terms & conditions

Bajaj Life Insurance Limited (Formerly known as Bajaj Allianz Life Insurance Company Limited) | IRDAI Reg no. 116

X

Terms & Conditions

I hereby authorize Bajaj Life Insurance Limited. to call me on the contact number made available by me on the website with a specific request to call back. I further declare that, irrespective of my contact number being registered on National Customer Preference Register (NCPR) or on National Do Not Call Registry (NDNC), any call made, SMS or WhatsApp sent in response to my request shall not be construed as an Unsolicited Commercial Communication even though the content of the call may be for the purposes of explaining various insurance products and services or solicitation and procurement of insurance business

%%Above illustration is for Bajaj Life eTouch- A Non Linked, Non-Participating, Individual Life Insurance Term Plan (UIN: 116N172V03) considering Male aged 25 years | Non-Smoker | Policy Term (PT)– 30 years | Premium Payment Term (PPT) – 30 years | Sum Assured opted is Rs. 1,00,00,000 | Online Channel | Standard Life | 1st Year Premium is Rs. 6,238. 2nd Year onwards premium is Rs. 6,659. Total Premium Paid is Rs. 1,99,349 | Medical Rates | Yearly Premium Payment Mode | Death benefit opted is lumpsum payout and monthly installments (Lumpsum Payout Percentage : 45, Income Payout Percentage : 55) | Premium shown above is exclusive of Goods & Service Tax/any other applicable tax levied, subject to changes in tax laws, and any extra premium and is for illustrative purpose only. This is inclusive of all the discounts mentioned above.

##Tax benefits as per prevailing Section 10(10D) and Section 80C of the Income Tax Act shall apply. You are requested to consult your tax consultant and obtain independent advice for eligibility before claiming any benefit under the policy.Above Tax benefit is calculated considering deduction of Rs. 150,000 and applicable tax rate of 31.20%.

@Term Insurance plan bought online directly from Bajaj Life Insurance has no commissions involved.

^^The Return of Premium amount is total of all the premiums received, exclusive of extra premium, rider premium and GST & /any other applicable tax levied, subject to changes in tax laws

Bajaj Life Insurance Limited (Formerly known as Bajaj Allianz Life Insurance Company Limited) | IRDAI Reg no. 116

X

Disclaimer

Bajaj Life eTouch- A Non Linked, Non-Participating, Individual Life Insurance Term Plan (UIN: 116N172V04)

*Tax benefits as per prevailing Section 10(10D) and Section 80C of the Income Tax Act shall apply. You are requested to consult your tax consultant and obtain independent advice for eligibility before claiming any benefit under the policy.Above Tax benefit is calculated considering deduction of Rs. 150,000 and applicable tax rate of 31.20%.

~Individual Death Claim Settlement Ratio for FY 2023-2024

1Premium Holiday has to be selected at inception to avail this benefit and also depends on other policy terms & conditions

Bajaj Life Insurance Limited (Formerly known as Bajaj Allianz Life Insurance Company Limited) | IRDAI Reg no. 116

Thank you for sharing your details. Our executive will get in touch with you shortly!

Ask for an Agent

Sign up for personal visit and tailored advice from our expert agents

ISO/IEC 27001:2022 Certified

ISO/IEC 27001:2022 Certified